To explain why the time is right for a building project, school board chairman Pat Flanders lists, in no particular order, the healthy economy, high employment rates, low interest rates, and equalization aid from the state of Minnesota.

The low interest rates not only help the economy in general but would have a direct influence on the project if the time comes for the school to issue bonds. Lower interest rates lowers the overall cost of the project, and consequently the local taxes.

Flanders said the school board thought interest rates were favorable in the early 1990s when the middle school was built. Now, he says, those rates are even better. Plus, equalization aid from the state would further defray the local cost.

Superintendent Howard Caldwell agreed, saying, "The state supports this issue by 46 percent. Only 54 percent of the cost at this time would be subject to local property tax."

"We want to be honest with the public, honest with the people. We want them to know exactly what they are getting into," added Caldwell. "We also feel the overall result of what we get versus the money we spend is of high value to our school as well as the community."

Equalization aid

Nearly ten years ago, the Minnesota State Legislature started the Debt Service Equalization Program to help "property poor" school districts. "Property poor" districts are determined by comparing the district's tax capacity to its student population. Based on the state formula, our local share of a building project is about 54 percent and the state share is 46 percent.

However, the state has a minimum threshold before the equalization aid takes effect. School districts must pay 12 percent of their tax capacity before equalization aid starts. For our school district this year, that means the first $405,000 in debt service must be paid, in full, by local tax dollars. The state pays 46 percent of the remaining debt service each year.

For the next 18 years, that is not a problem as the district's bond issue from the 1992 building project will continue to be on the tax rolls until the 2017-2018 school year. The school district already pays between $600,000 and $700,000 each year in debt payments on that building project, more than enough to meet the minimum threshold. "On the new debt, they're going to get that 46 percent without meeting that threshold," explained Carolyn Drude, who works on the education team for the district's financial advisor, Ehlers and Associates.

The state aid is paid gradually, over the life of the bond issue. The school district issues the bonds, and the state helps with interest and principal payments each year. Already, the school district receives debt aid from the state, just over $100,000 each year, to retire the 1992 bonds.

As equalization aid from the state is based on tax capacity and student population, the rate could fluctuate, depending on those two factors.

Both Flanders and Drude said the state legislature is committed to debt equalization. Flanders explained that the program resulted from a class action law suit demanding equity in educational opportunities. The legislative fix, he said, was the result of a mandate from the judicial branch. "That's what makes me much more confident about this," he said. "It's not up to the whim of the legislators."

Duration of the bonds

To qualify for the state equalization aid, the school district needs to issue bonds for at least 20 years. Ehlers and Associates has proposed a 20-year bond issue that would wrap the payments around the existing debt.

(The financial figures, based on projections by Ehlers and Associates, can not be figured exactly until the actual bonds are bought and the actual interest rate is known. For their projections, an interest rate of 5.7 percent was assumed.)

Using this approach, the district's overall debt payments over the next 20 years would be kept uniform. The overall levy would be about $910,000 per year, including the 1992 bonds as well as the current issue. With state aid contributing about $235,000 each year, the local levy will be for about $675,000 each year.

For the first 17 years, payments on the new debt are projected to amount to a quarter of a million dollars each year, without the state aid. In the last three years, the entire debt levy, about $910,000 each, would retire the principal on this issue.

In the last three years of this bond issue, after the 1992 bond issue is paid off, the minimum threshold payments would need to come solely from the auditorium and fitness center bond issue. The state still would pay 46 percent after that threshold, but their overall contribution would be at a lower percentage.

With interest included, over the 20 year life of the bonds, the building proposal would cost about $6.8 million, with the state contributing $2.6 million and the local portion being $4.3 million. In all, the state would pay for two-fifths of the auditorium and fitness center.

Local taxpayers would end up paying approximately $125,000 extra each year in the first 17 years of the bond issue. In the last three years, our entire debt service payment, about $675,000 in local funds each year, would pay for the auditorium and fitness center.

Our school district has a statutory bond limit of just over $29 million. With $7 million still outstanding from the 1992 project, the current proposal would leave us almost $19 million below that limit. "Even with $3.4 million," explained Caldwell, "we'd be quite a ways from that (limit)."

The school district is also in the first year of a ten-year excess levy for operating funds. Each year, the district will levy $315 per pupil unit, which is based on the student population, with weighting for their grade levels. "Believe me," said Caldwell, of the excess levy, "we need to have it."

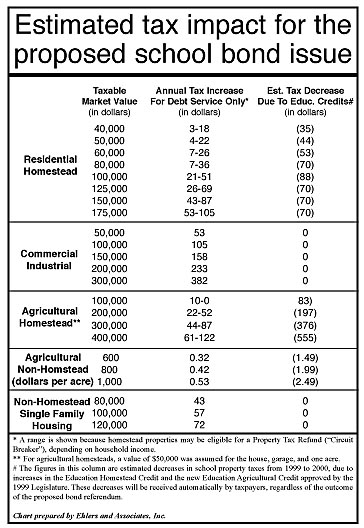

Estimated tax impact

A chart of the estimated tax impact on school district residents can be found in the colored box on the front page. Worksheets for computing your estimated tax liability for this bond issue are in the box on this page. Both were prepared by Ehlers and Associates. Anyone with questions can call Ehlers and Associates at 651-697-8500 and speak with a member of the education team.

On that chart, the second column, labeled "Annual tax increase for debt service only," indicates the projected increase for various property owners. The increase due to this proposed bond issue is the higher figure.

The lower figure is for those property owners who qualify for a Property Tax Refund, also known as the "circuit breaker." To be eligible for this refund, homeowners or farmers must have an annual income of less than $68,500, according to Ehlers and Associates. An application must be made to the state for property tax relief. The maximum refund for homeowners is $490. Up to 80 percent of the taxes from this bond issue could be refunded to eligible property owners.

For example, a residential property worth $60,000 would have an estimated tax increase of $26 for the proposed bond issue. If the homeowner qualified for the Property Tax Refund, that increase might be reduced to $7.

The last column on the front page chart, labeled "Estimated tax decrease due to education credits," shows the amount taxes are expected to decrease next year due to two state tax credits. Homeowners, both residential and agriculture, get credit on their taxes, which should be automatically deducted from your tax bill. The credit for next year has been raised again, yielding a savings to homeowners compared with last year's taxes.

To continue our example, that homeowner of a $60,000 property would have his taxes reduced for next year by $53 through the Education Homestead Credit.

Agricultural property owners will receive a similar credit starting with taxes paid in the year 2000. An unlimited credit will be given to both homestead agricultural property and nonhomesteaded property. Homestead property receives credit at a slightly higher rate.

Both homeowners and farmers can expect tax decreases next year. "The relief is not as great because of the extra burden we're asking of property owners," said Caldwell.

On the other hand, businesses and recreational housing would face the tax increase of the bond proposal without any tax credits. "The one thing I can say to seasonal and recreational people is this is one thing that they might use," said Flanders, referring to the expected community use of the auditorium and fitness center.

Comparison with 1992

Flanders pointed out that business owners would not be hit as hard as they were by the $7.9 million bond issue in 1992. Back then, a $100,000 business faced a tax increase of $880. This time, the projected increase is only $105. For a $200,000 business in 1992, the tax increase was nearly $2,200. This time, it is projected to be just $233.

"When you compare charts, it's ten percent (of the tax increase) compared with last time," explained Flanders.

That $60,000 house in 1992 faced a tax increase of $165. Even with the Property Tax Refund, the burden was still $74.

An agriculture homestead valued at $200,000 would have an estimated tax increase this time of $52. In 1992, their taxes were increased about $635.

Flanders said the building project in 1992 was supported despite these tax increases, because of the need of the district. "That was a much more noticeable sacrifice," he said.

(Michael Jacobson served as a member of the Facility Task Force, the committee that researced and designed the building proposal.)

{kind=link}